Fix and Flip for Beginners: What HGTV Doesn't

Show You

Author • Hunter Foote

JUNE 5, 2026

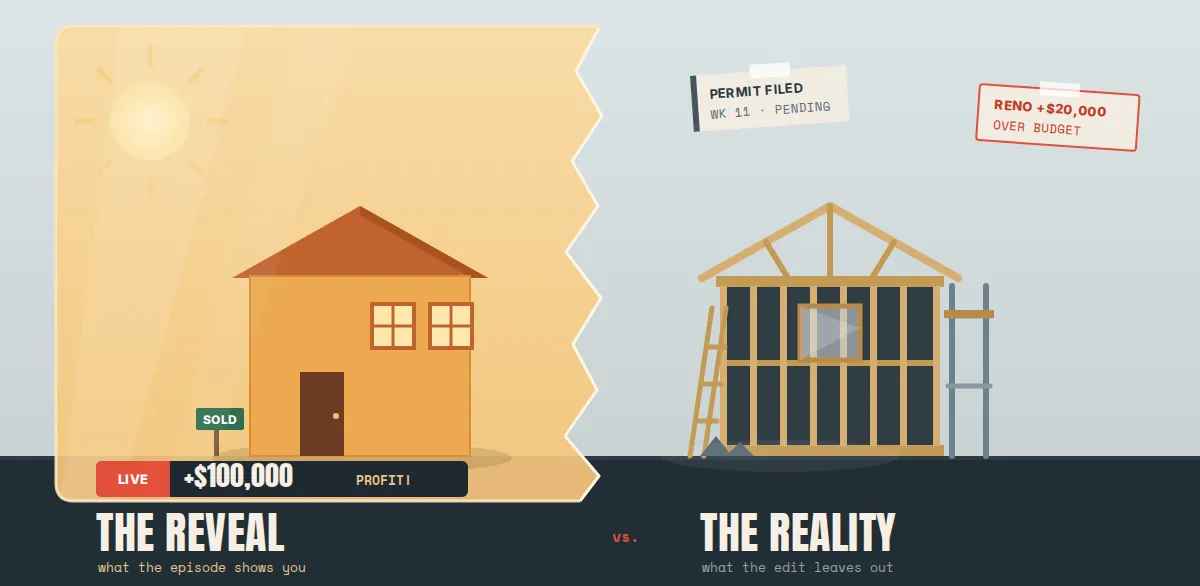

You know the show. Someone buys a tired house, there's a montage set to upbeat music, a few tense moments about a budget, and then the reveal, gleaming floors, an open-concept kitchen, and a smiling host announcing a $90,000 profit. Roll credits. The whole thing wraps in what feels like an afternoon.

Now here's what the episode left on the cutting-room floor: the permit that took eleven weeks to approve, the contractor who vanished for a month, the rotted subfloor nobody priced in, the two mortgage payments made on an empty house, and the buyer who offered $40,000 under asking because the market cooled while the cameras were off. The reveal is real. The profit check is sometimes real. But the tidy, low-stress, money-printing version of house flipping is television, and television is in the business of editing out the parts that would make you nervous.

This is the unedited version. If you're exploring fix and flip for beginners, this post covers what the strategy actually is, where the money is genuinely made and lost, what the real timeline looks like, and the risks that quietly end most first deals. It's not meant to scare you off. Plenty of people build real wealth and do genuinely good work flipping houses. It's meant to make sure you walk in with your eyes open.

What Fix and Flip Investing Actually Is

Fix and flip is the strategy of buying a property in distressed or underperforming condition, improving it, and reselling it, usually within a year. You're not buying to keep it. You're buying to transform it and move on.

It's a short-term, value-add play: you add value to a property and capture that value at sale. (If you've read our earlier posts on value-add investing, this is that concept compressed into a tight timeline.) That's what separates it from buy-and-hold investing, where the goal is steady, ongoing rental income over years. Fix and flip is built for a single lump-sum profit when you sell, one transaction, one payday, then on to the next.

That distinction matters more than it sounds, because it changes everything about how you evaluate a deal. A buy-and-hold investor asks, "Will this cash flow every month?" A flipper asks a sharper, riskier question: "Can I buy, fix, and sell this for more than it costs me to do all three, and do it fast enough that time doesn't eat the profit?" Understanding that question is the foundation of fix and flip investing.

Where the Profit Is Actually Made and It's Not the Renovation

Here's the single most important idea in this entire post, and it's the one HGTV gets exactly backward: the profit in a flip is determined at acquisition, not at renovation.

The show makes it look like the granite countertops and the dramatic backyard reveal are where the money comes from. They're not. The renovation is the mechanism that unlocks value but the actual margin was won or lost the day you agreed on a purchase price. Buy the property right, and a competent renovation prints the profit. Overpay at the start, and no amount of beautiful tile work will save the deal.

That's why overpaying for the property is the number one reason first-time flippers lose money. They fall in love with a house, get into a bidding contest, and pay a price that leaves no room for the surprises that always come.

So the investor's real job at acquisition is to work backward. You start with the after-repair value (ARV) simply, what the property will be worth once renovations are finished, based on comparable sold properties in the area. Then you estimate your renovation costs honestly (emphasis on honestly). Then you subtract a margin for profit and risk. What's left is the most you can pay. If the seller won't meet that number, you walk. House flipping basics start and end with the discipline to walk away from a deal that doesn't leave margin.

The Real Deal Timeline This Is Not a 6-Week Project

The montage compresses months into minutes. Real flips don't compress. Here's roughly how the calendar actually unfolds:

Subtract debt service from NOI and you get the number you actually feel in your bank account: cash flow.

Acquisition: finding, analyzing, offering, and closing weeks, sometimes longer.

Permits and contractor scheduling: pulling permits and getting a crew lined up weeks to months, and largely outside your control.

Renovation: the actual work weeks to months depending on scope.

Listing and sale: marketing, showings, offers, and closing with the buyer weeks to months.

Add it up and a well-run flip realistically takes four to nine months from purchase to final sale. A poorly run one, bad contractors, permit delays, a slow market, can stretch past twelve.

Why obsess over the timeline? Because every extra month costs you money even when nothing is being built. Those are carrying costs, the mortgage payment, property taxes, insurance, and utilities you pay the entire time you own the house. A house sitting half-finished is a house quietly draining your budget. That's why, in fix and flip investing, speed isn't just an advantage, it's a discipline. The investors who win treat the calendar as ruthlessly as they treat the budget.

The Three Risks That Kill Most First Deals

When a first flip goes wrong, it's almost always one of three risks and the real danger is how they feed each other.

Risk 1 — Timeline overruns. Contractors miss deadlines. Permits stall. You open a wall and find structural problems nobody knew about. Every delay pushes your sale date further out.

Risk 2 — Cost overruns. Renovation budgets swell. Material prices come in higher than your estimate. "While we're at it" scope creep turns a kitchen refresh into a gut. Each overrun chips directly at your margin.

Risk 3 — Market shifts. The property that would have sold for your ARV when you bought it may be harder to move by the time you're done. Interest rates rise, buyer demand softens, and the number you underwrote no longer holds.

Now the crucial insight: these risks compound. A timeline overrun piles on carrying costs. A cost overrun eats into margin. And a market shift can swallow whatever's left. One problem is survivable. Two at once is where first-time flippers get hurt. This is exactly why you build margin at acquisition, it's the cushion that absorbs the surprises.

A Hypothetical Deal Walked Through

Let's make it concrete.

⚑ The following is illustrative only round numbers chosen to show the mechanics. It is not a typical or guaranteed outcome.

Line Item

Purchase price

Renovation cost

Carrying costs (financing, taxes, insurance, utilities)

Broker commission and sale costs

Total all-in cost

Sale price (at ARV)

Gross profit

Amount

$500,000

$80,000

$20,000

$20,000

$620,000

$720,000

$100,000

On paper, that's a clean $100,000 and that's the version that makes it to TV.

Now watch how fast it changes. Say the renovation runs $20,000 over budget (a common, almost mild overrun). Your all-in cost climbs to $640,000 and your profit drops to $80,000. Now add a softening market, so the house actually sells for $30,000 less than your ARV $690,000 instead of $720,000. Your profit falls to $50,000. Two ordinary, realistic surprises just cut your gross profit in half. Add a serious timeline overrun on top, with several more months of carrying costs, and you can see how a "$100,000 deal" becomes a break-even or worse. That's not a doomsday scenario. That's a Tuesday.

Is Fix and Flip Right for You?

Before you chase your first deal, be honest about what it demands:

Capital. You need money for the acquisition, the renovation, and the carrying costs and a reserve on top for the surprises.

Time and attention. Managing contractors, timelines, permits, and budgets is a job. It rewards people who show up and stay on top of details.

A high tolerance for things going wrong. Something always does. The question is whether you have a plan for when it does, and the temperament to stay calm and solve it.

Active involvement. This is the opposite of passive. Fix and flip is hands-on work, not a set-it-and-monitor-it investment.

Personality fit is real here. People who genuinely enjoy problem-solving and project execution tend to thrive. People who want their money working quietly in the background usually don't and there's no shame in that. Knowing which one you are is itself a smart investment decision. If you're still learning how to flip a house for beginners, the honest first step is deciding whether the work actually suits you.

A Kingdom Note on Fix and Flip Value Creation vs. Extraction

There's a version of flipping that's genuinely good work. You take a deteriorating house that's dragging down a block, and you make it sound, livable, and beautiful again. A family moves in. The neighborhood lifts a little. That's real value creation you left the world slightly better and got paid for doing it.

There's also a version that's purely extractive: cutting corners behind the walls where inspectors won't look, ignoring the neighborhood's character, or letting a buyer assume the house is something it isn't. The numbers might work, but you've taken value rather than created it.

We hold ourselves to one simple test: Would we be comfortable if the buyer knew exactly what we did, how we did it, and what we charged? If the answer is yes, we're building something. If it's no, we're not no matter what the spreadsheet says. That standard costs a little margin sometimes. It's worth it every time.

The Key Takeaway

Fix and flip can be a legitimate, profitable, and even meaningful form of real estate work. But it is not easy, it is not fast, and it is not forgiving of a bad purchase. The investors who do it well share three habits: they buy right, they manage timelines ruthlessly, and they build enough margin to survive the surprises that the TV edit never shows. Get those three right, and flipping becomes a real strategy. Get the first one wrong, and the other two can't save you.

What's the one thing about fix and flip you didn't fully understand before reading this and does it change your interest level? That answer is worth sitting with before you go looking for your first deal.

✦ Free course + community access

Join the mailing list & get instant access.

Drop your email and we'll enroll you in the free course and the community, plus send occasional teaching and updates.

No spam — just value for Kingdom builders.

First name

Your first name

Email address

Your email address

By joining you'll be enrolled in the free course & community.

Free, Bible-rooted real estate education for

Christian entrepreneurs called to steward,

build, and bless.

EXPLORE

GET STARTED

Built to Bless is founded and supported by the Vanderburgh Foundation, Inc., a 501(c)(3) nonprofit. All donations are tax-deductible to the fullest extent allowed by law.